This article is one of a series of SuperMail articles by Mr. Colin Grenfell, who is a superannuation consultant, an actuary and Associate Director of SuperEasy.

Each article compares the long term performance of two investment sectors, such as Australian Shares, International Shares, Property, Fixed Interest or Cash, or financial indicators, such as the Consumer Price Index (CPI), Average Weekly Ordinary Time Earnings (AWOTE), 90 day Bank Bill Rates or 10 year Bond Rates.

- This article compares:

- the investment performance of a diversified "Balanced" portfolio, with

- rates of salary increases (as an indicator of changes in living standards) over the 43 years from 30 June 1965, when suitable data for the various investment sectors first became available, to 30 June 2008. The article is an update of a similar article published over five years ago. The salary increases used are obtained from published Average Weekly Ordinary Time Earnings (AWOTE) since 31/12/74 and Average Weekly Earnings (AWE) prior that date.

The Balanced portfolio comprises:

| Growth Assets (70%) |

36% Australian Shares | Income Assets (30%) |

16% Fixed Interest |

| 25% International Shares | 7% International Bonds | ||

| 7% Listed Property | 5% Cash | ||

| 2% Direct Property | 2% Inflation Linked Bonds |

Let's examine what happened if $10,000 was invested at the start of the period, assuming that all investment income (i.e. dividends, net rent and interest) was reinvested back in each sector, as occurs with some managed investments. The portfolio is revalued monthly based on market values. For comparison the salary (AWOTE and AWE) index starting from a base of $10,000, is also shown.

The following chart plots the results for the 43 year period. The chart has been prepared using a logarithmic scale designed to show proportional increases and decreases in values (rather than changes in the values in dollar terms). The ratio of the Balanced Portfolio results as a percentage of the Salary Index results is also shown. During most of the latter part of the 43 year period the rate of investment return was significantly more than the rate of salary increases.

The next table summarises the 43 year results:

| $10,000 invested for 43 years from 30/06/1965 to 30/06/2008 Accumulated to: |

Balanced Portfolio $640,390 | Salary Index $234,760 | "Gap" | |

| Average annual | First 21 yrs | 10.61% | 10.67% | -0.06% |

| Compound return | Next 22 yrs | 9.72% | 4.77% | 4.95% |

| 43 yrs | 10.16% | 7.62% | 2.54% | |

The 'gap' is the average annual investment return in excess of salary increases (eg 10.16% less 7.62% equals 2.54%). On a compound basis the actual real (salary-based) average investment return is 2.36% pa (ie 1.1016/1.0762 less 1 equals 2.36%). A long term positive real investment return is critical for the funding of adequate retirement benefits.

The year by year investment returns for each year ending 30 June have been:

The rate of increase in AWOTE for the year ending 30 June 2008 has been assumed to be 4.7%. This is an estimate based on the annual rate of increase in AWOTE to February 2008. Note that the annual returns for the Balanced portfolio were negative 7 times in the 43 years. More importantly, from a superannuation funding perspective, the annual returns for the Balanced portfolio were less than salary increases 13 times in the 43 years.

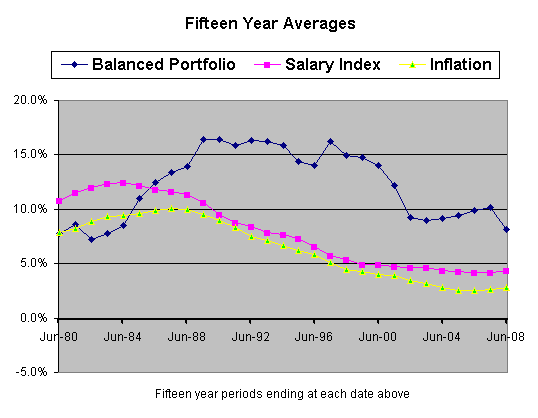

To give an indication of trends over the period, the next chart plots the 15-year moving average compound returns per annum. The 15-year moving average compound rate of inflation per annum, based on changes in the CPI, is also shown.